Latest reports indicate that the tourism boom continues unabated with Dubai hotels registering an 83.6% occupancy rate last year – with more of the same on the plate in 2013. More impressive was the climb in both RevPAR (revenue per available room) and Average Room Rates both up by 10.4% and 7.3% respectively.

Latest reports indicate that the tourism boom continues unabated with Dubai hotels registering an 83.6% occupancy rate last year – with more of the same on the plate in 2013. More impressive was the climb in both RevPAR (revenue per available room) and Average Room Rates both up by 10.4% and 7.3% respectively.

The buoyancy in the market is reflected by the likes of Hilton and Marriott planning to add a further 1,000 and 3,000 rooms to their Dubai inventory over the next two years. Furthermore, the Jumeirah Group have started work on Phase 4 of Madinat totalling US$ 680 million whilst Al Habtoor will be building three more hotels on its Metropolitan site.

One event this week that saw the hotels bursting at the seams was Gulfood. With some 4,200 exhibitors and 60,000 visitors, the 4-day event is now the largest food exhibition in the world. For such a small city, it is a surprise to some that Dubai has over 2,000 companies involved in the food and beverage sector. Indeed it is estimated that almost 15% of Dubai’s manufacturing is food-related.

With its 2012 passenger numbers jumping 13.2% to 57.7 million, Dubai International Airport recorded a massive 14.6% hike in January numbers to 5.6 million compared to twelve months earlier. Despite the slowdown in world trade, the emirate once again bucked the trend with an 8.6% increase in freight traffic to 189k tonnes. (Near neighbour, Abu Dhabi dealt with 1.3 million passengers and 49k tonnes).

The driving force behind this phenomenal growth is Emirates which has carried 18.7 million passenger since last April – an increase of 15.4%. No wonder that pundits are expecting stellar profits when results are released in April. Their September 2012 half year figures indicated a doubling of its Net Income to US$ 463 million.

Troubled developer, Nakheel, is slowly battling back from its massive arrears problem and, with this week’s US$ 56 million repayment, has now settled US$ 252 million since its August 2011 US$ 16 billion debt restructuring scheme. Since then the company has delivered around 4,000 units and has a further US$ 380 million of developments in the pipeline. Last month, it reported that it had seen its 2012 Revenue surge 91% to US$ 2.13 billion.

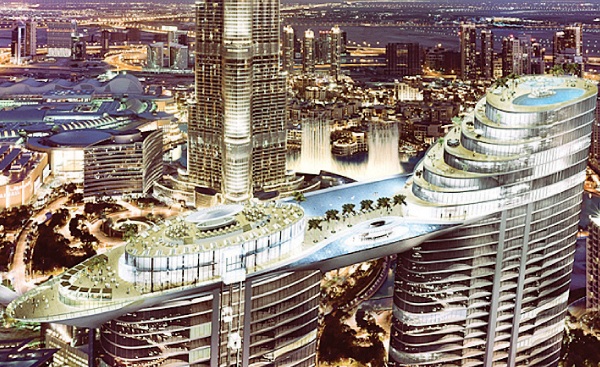

Hardly a month goes by without Emaar Properties announcing a new project. This time it is a 189-room hotel and 532 serviced apartments located in Downtown. The Address Residence Sky View will be 230 metres high and have 50 floors. Sales will start on 02 March and it does not take a clairvoyant to see that it will be sold out the same day.

The largest listed contracting company in Dubai had a turbulent week. Arabtec announced that both its Chief Executive (and founder some forty years ago), Raid Kamal, and CFO, Ziad Makhzoumi, were no longer with the company. It did not take long for Abu Dhabi-based Aabar, who bought 22% of the company in August 2012, becoming its major shareholder, to overhaul the boardroom. On the financial side, the 2012 Profit fell 37% to US$ 37.9 million and it announced that it plans to increase its capital by US$ 1.77 billion via a rights issue (US$ 1.31 billion) and convertible bonds (US$ 463 million). The market did not take too kindly to the news with the stock losing 9.8% on Thursday to close at US$ 0.728.

Empower, the district cooling services provider, registered a 17% rise in 2012 profits to US$ 51.8 million with assets of US$ 1.23 billion. It has also managed to reduce its loan book from US$ 354 million to US$ 131 million. Dubai’s population growth over the next five years is the main reason why industry analysts expect the UAE district cooling industry to triple from US$ 4.09 billion to US$ 12.26 billion.

The Dubai government has bought back US$ 834 million of its own Medium Term Note of US$ 1.77 billion issued in April 2008. There is an apparent move afoot to better manage outstanding liabilities in the light of changed circumstances and lower borrowing costs.

Last month, HH Sheikh Mohammed bin Rashid Al Maktoum, spoke about his desire to make Dubai the hub for global Islamic economy. Although difficult to quantify, the global value of sukuk (Islamic bonds) is in the region of US$ 400 billion of which only 2.25% emanates from Dubai – well behind the likes of the big two (London US$ 27 billion and Malaysia US$ 23 billion). Last year, there was a 42.3% surge in the issues of sukuk to US$ 121 billion. On Wednesday, the Dubai ruler reiterated his ambition that Dubai become the number one global centre for such financing.

The Dubai Financial Market Index ended the week at 1927 nudging marginally higher from its Sunday opening of 1923. In the first two months of the year, the Index has risen by 18.77%.

With the political impasse continuing on Capitol Hill, the US is once again teetering on the edge of its fiscal cliff. With no imminent deal in sight, it seems likely that US$ 85 billion worth of spending cuts are due to take place. Although this seems a high figure, it is not when compared to the federal expenditure of US$ 3.8 trillion.

It was a bad start to the week for several European economies none moreso than the UK and Italy. Moody’s became the first ratings agency to downgrade the Cameron-led economy from AAA to Aa1 because of worries about the lack of growth prospects and, to a lesser extent, its relatively high levels of debt. Apart from the economic impact, it will lead to a political bun fight that may see the demise of the Chancellor George Osborne.

Italy, the world’s eighth largest economy, is in a more perilous state, not helped by political uncertainty following the recent general election. It has had six straight quarters of recession with the economy contracting 0.7% in Q4 and 2.7% in 2012. The unemployment rate has risen from 8.9% to 11.2% over the past twelve months with the situation expected to worsen in 2013. No wonder its borrowing costs have started to climb again with the latest sale of 10 year bonds up from 4.17% to 4.83%. Its debt position now is in excess of US$ 2.7 trillion whilst the unemployment rate continues to rise – up from 8.9% to 11.2% in 2012.

Reality has finally hit home for the EU bureaucrats. Like King Canute, they now realise that the tide cannot be turned and have conceded that the eurozone will be in recession in 2013. It was only in December that growth was forecast for this year but a combination of high unemployment and banks diving for cover and not lending, means that the bloc will remain in the doldrums for at least another year.

It has now dawned on authorities that joblessness is probably its main long-term problem and the fact that over 19 million are not working will continue to drag the eurozone deeper into economic trouble. At the same time, interest rates are at historical lows but that means nothing to public and private consumers if the banks are not lending.

Banks are again in the news for all the wrong reasons. Four UK banks have already put aside US$ 19.3 billion as a provision for future compensation claims for mis-selling payment protection insurance (PPI) to its long suffering customers. Lloyds TSB, Barclays, RBS and HSBC have provided US$ 9.9 billion, US$ 3.9 billion, US$ 3.3 billion and US$ 1.6 billion.

One of those offenders, RBS, has managed to make a loss every year since the UK government paid US$ 104 billion in 2008 to save the bank and become an 81% shareholder. In 2012, it managed to more than quadruple its loss to US$ 7.8 billion and then still want to pay out bonuses totaling US$ 921 million!

Not to be outdone, the world champions, Spain, have gone one better. Having received US$ 24.3 billion EU bailout funds in May 2012, one nationalised bank, Bankia, has returned an annual loss of US$ 25.2 billion. Next week, two other government-owned banks, Catalunya Banc and NCG Banco will come in with losses topping US$ 26 billion whilst Banco Popular and Banco de Valencia have already recorded 2012 deficits of US$ 3.3 billion and US$ 4.7 billion.

Money for Nothing